The upside is real. Africa is becoming the world’s largest source of new workforce entrants; critical minerals remain a critical opportunity; and there is a significant pool of under-utilised African capital. But two risks still set the terms for everything else: expensive financing and political instability. The five dynamics described below frame the 2026 outlook in practical terms: what to watch, where value can be built and what needs to change to unlock long-term investment.

Africa’s 500% premium

Analysis by One Data shows that borrowing from capital markets is costing African governments around 500% of what it would have cost to borrow the same through World Bank financing. This premium added $56bn in additional costs on capital-market debt raised in the five years prior to 2021.

If this “Africa risk premium” isn’t reduced, debt service will continue to crowd out public investment – and private credit will stay scarce and expensive, even in fast-growing markets.

The path to change is structural: better data and transparency; reforms to how Africa is priced; and perceived; and practical steps that make the global financial system work for African issuers (not against them).

Markets are pricing in long-term coup risks

December’s coup in Guinea-Bissau is the ninth unconstitutional power takeover in West and Central Africa in the past five years. This is priced into Africa’s higher cost of capital, with long-term consequences.

After a failed coup attempt in Benin, the sharpest bond declines were in longer-dated maturities – a sign that investors were repricing long-horizon political uncertainty, not just near-term liquidity.

For 2026, investors should pay attention to the trajectory of stability. They should look for whether transitions resolve with credible electoral timelines; whether regional bodies can restore deterrence; and whether insecurity concentrates along key trade and commodity corridors, pushing up logistics and insurance costs.

Taken together, instability and financing costs have outsized influence over Africa’s most valuable resources: human, natural and financial.

Africa is the world’s talent pipeline

By 2030, half of all new entrants into the global labour force will come from sub-Saharan Africa. Job markets are struggling to keep up.

For every two people added to Congo’s working-age population between 2005 and 2020, only one job was created on average – a pattern repeated across Nigeria, Ethiopia, and other large states.

This is where demographics meets financing. Job creation depends on making it easier for firms to grow. Starting with reliable, affordable energy, and a more level playing field on taxation, the cost of capital and regulation. When borrowing is structurally expensive, the job-enabling investments get delayed.

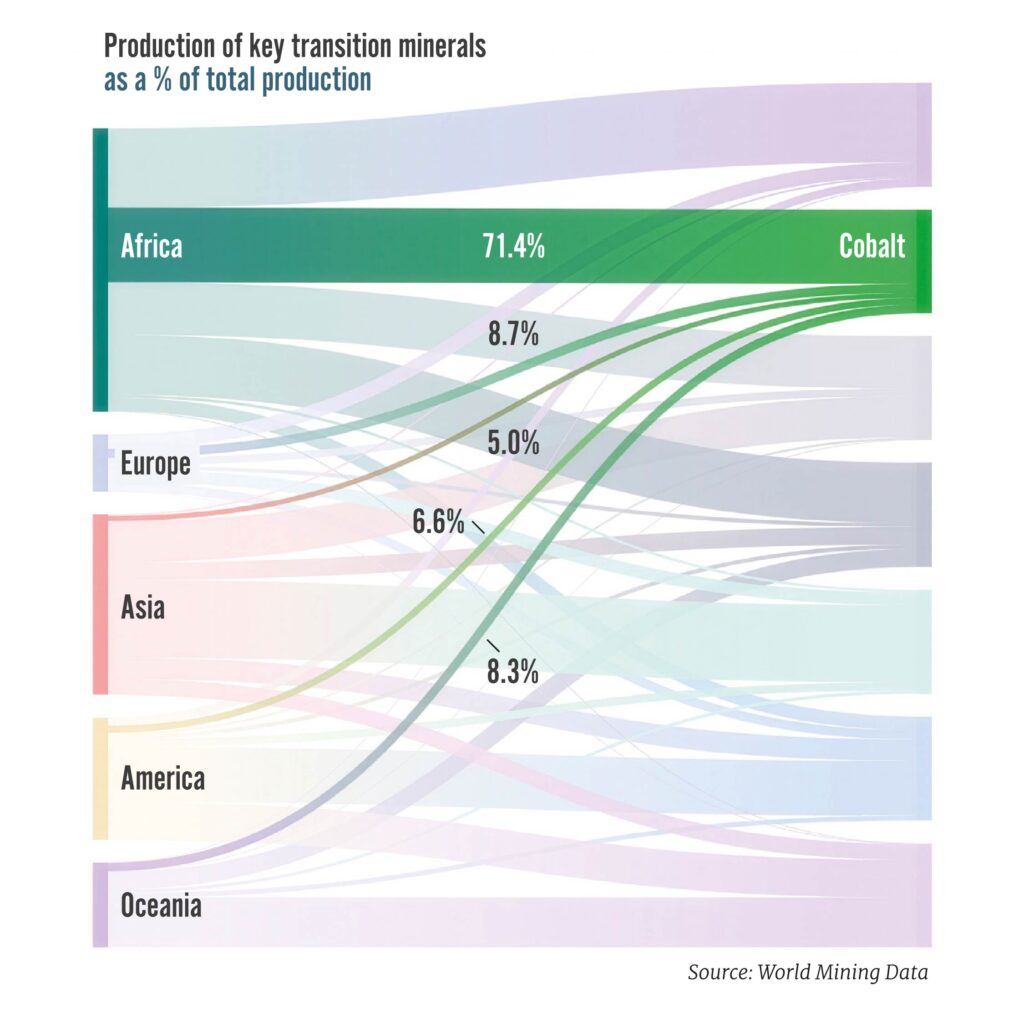

Cobalt gives Africa leverage in the energy transition

The DRC accounts for over 70% of global cobalt production and has moved to a quota regime – permitting export of 96,600 tonnes a year in 2026 and 2027 – to manage supply and strengthen state revenues. But in eastern Congo armed groups including M23 have used illicit mining and smuggling networks to raise funds, draining public revenues and undermining efforts to bring the sector under stronger oversight.

The result is a familiar trap: the places where improved security and governance are most needed are often the hardest for investors to back, leaving the system vulnerable to leakage.

This is a chance to turn a strategic resource into jobs, stronger public revenues and more resilient growth – but only if the value doesn’t slip away through raw exports and illicit trade.

Today, the pattern is still “mined in Africa, processed elsewhere”.

The 2026 test is whether DRC’s quota regime becomes predictable and enforceable and whether partners and investors back practical improvements – stronger standards, more transparency in supply chains, and more in-country value addition – so communities see safer work, better returns and broader opportunity, not just higher prices.

Africa has domestic capital waiting to mobilise

The Africa Finance Corporation estimates that Africa holds roughly $4 trillion in domestic capital across pension funds, sovereign wealth funds and banks – which could be redirected into infrastructure and productive investment.

So the continent doesn’t only need more foreign capital; it needs to convert its own pools into investable, long-duration finance.

But shallow capital markets, limited project pipelines, credit-risk constraints and governance concerns keep funds in limbo.

Africa also needs to reduce the leakage of wealth being stored or invested outside local economies: a report by the Political Economy Research Institute at the University of Massachusetts Amherst estimates $2.7 trillion in capital flight from 30 African countries in the years 1970 to 2022, averaging $97bn a year since 2010.

Better data is now a competitiveness issue

All this points to a core problem: big shifts get priced quickly, often on partial or outdated information. Fragmented or incomplete data can amplify perceived risk and keep borrowing costs high; it can lead to inefficient resourcing decisions.

That’s why work is underway in the ecosystem to build more credible, comparable evidence on African investment performance, development finance flows and the impact of these investments. n

This page is part of a new partnership between African Business and One Data, which aims to “assemble standardised, business-ready information – covering debt, health, climate and development finance, the cost of capital and more” to provide data-driven insights on Africa.

Visit data.one.org for more information.